Getting preapproved before visiting a dealership could save buyers thousands of dollars on interest and fees

Buying a car is exciting until the financing conversation begins.

For most Americans, paying cash for a vehicle is unrealistic, which means choosing the right auto loan becomes one of the most important parts of the purchase.

The biggest question buyers face is simple:

Should you finance through the dealership or get a loan directly from a bank or credit union?

The answer depends on your credit score, loan offers, incentives, and how prepared you are before walking into the showroom.

Why Banks Often Offer Better Loan Rates

Many financial experts recommend starting with a bank or credit union preapproval before visiting a dealership.

This gives buyers:

- A clear spending limit

- Better negotiating power

- A chance to compare rates

- Protection from overpriced financing offers

According to the Consumer Financial Protection Bureau, direct lenders like banks and credit unions frequently offer lower interest rates than dealership-arranged financing.

For buyers with strong credit, rates from banks can sometimes drop below 5% APR, depending on the lender and market conditions.

Preapproval also helps shoppers focus on the vehicle’s actual price instead of being distracted by low monthly payment tricks.

Why Dealers Push Financing So Hard

Dealership financing is convenient because buyers can handle the entire process in one place.

In many cases, the dealer sends your application to multiple lenders and returns with loan options quickly.

However, there is a catch.

Dealers often earn money by increasing the interest rate above the lender’s original approval rate.

That markup can increase the total amount paid over the life of the loan.

Still, dealership financing is not always the bad option many people assume.

Manufacturers sometimes offer:

- 0% APR promotions

- Cashback incentives

- Bonus discounts

- Special lease deals

Those promotions can occasionally beat traditional bank financing.

Smart Buyers Compare Both Options

Financial experts consistently recommend the same strategy:

- Get preapproved through a bank or credit union

- Bring that offer to the dealership

- Ask the dealer to beat it

This approach gives buyers leverage during negotiations and helps prevent overpaying.

Many experienced car shoppers on Reddit also recommend keeping outside financing ready before entering negotiations.

In some cases, dealerships may lower the car price further if buyers agree to finance through them.

That means the best deal is not always the lowest APR alone.

Monthly Payments Can Be Misleading

One of the biggest mistakes buyers make is focusing only on the monthly payment.

Dealers can stretch loans to:

- 72 months

- 84 months

- Or even longer

This lowers the monthly bill but increases total interest costs dramatically.

According to MarketWatch, long-term car loans are becoming increasingly common as vehicle prices continue rising past $50,000 on average in the U.S.

A lower monthly payment may sound attractive, but buyers can end up paying thousands more over time.

Experts recommend paying attention to:

- Total loan cost

- Interest rate

- Loan term

- Down payment

- Fees and add-ons

Credit Unions Continue To Gain Popularity

Many consumers are turning to credit unions for car financing because they often provide lower rates and more flexible approval standards.

Online discussions among car buyers frequently point to credit unions as one of the best places to secure competitive financing.

Unlike dealerships, credit unions also tend to have fewer hidden fees and less pressure to purchase extras like extended warranties or GAP coverage.

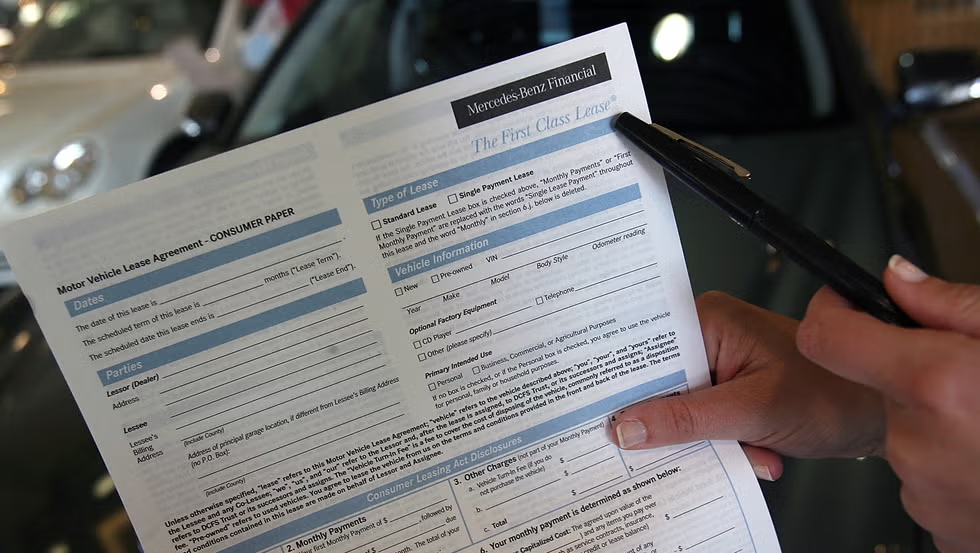

The Finance Office Is Where Buyers Lose Money

After agreeing on a car price, buyers are usually sent to the dealership’s finance office.

This is where many extra costs appear.

Common upsells include:

- Extended warranties

- Tire protection packages

- GAP insurance

- Maintenance plans

- Paint protection

According to Car and Driver, buyers should carefully review every document before signing because hidden charges can easily increase the total purchase price.

Walking away is always an option if the numbers suddenly change.

The Best Strategy Before Buying A Car

The most financially secure approach is usually:

- Check your credit score first

- Compare rates from multiple lenders

- Get preapproved before shopping

- Negotiate the vehicle price separately

- Review the full loan cost carefully

Experts say buyers who prepare financing in advance typically have stronger negotiating power and avoid costly mistakes.

With car prices and interest rates remaining high across the U.S., understanding how financing works can save consumers thousands of dollars over the life of an auto loan.